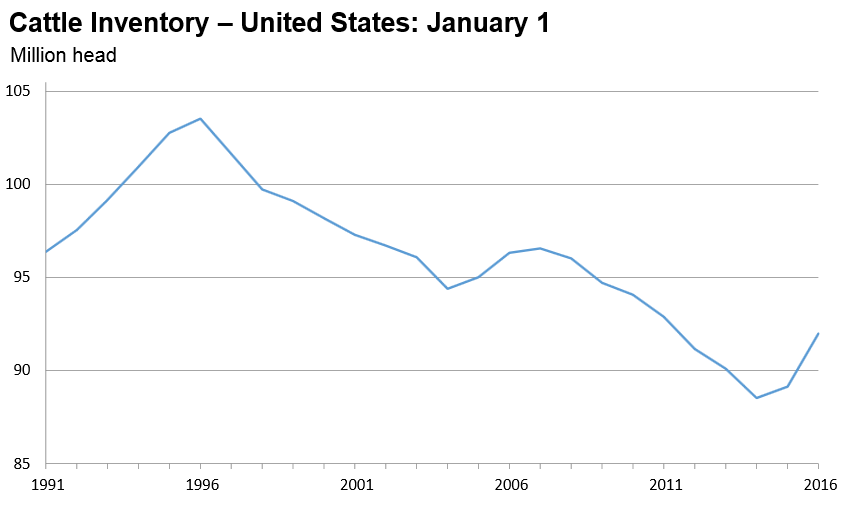

Much of the agricultural economy in the country is driven by the basic economic principles of supply and demand. Why are commodity prices for crops grown in the Southeast so low? For the most part it is related to an increase in the supply (production) and a reduction in demand from foreign exports due to the strong U.S. Dollar. The one bright spot the past several years has been beef cattle prices. This is changing however, and the recent report from USDA on total cattle inventory in the U.S. confirms that the beef herd is definitely rebuilding. The following are the highlights of USDA’s recent report on the U.S. Cattle Inventory for January 1, 2016.

January 1 Cattle Inventory Up 3 Percent

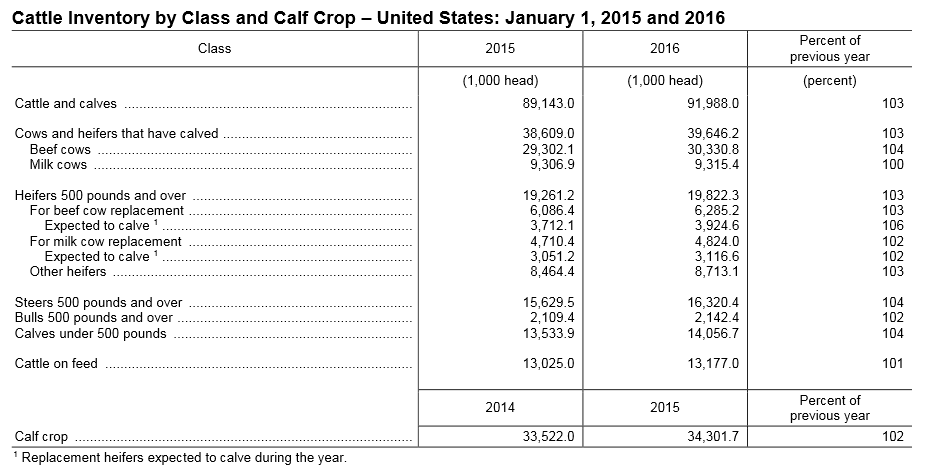

- All cattle and calves in the United States as of January 1, 2016 totaled 92.0 million head. This is 3 percent above the 89.1 million head on January 1, 2015.

- All cows and heifers that have calved, at 39.6 million head, are 3 percent above the 38.6 million head on January 1, 2015. Beef cows, at 30.3 million head, are up 4 percent from a year ago. Milk cows, at 9.32 million head, are up slightly from the previous year.

- All heifers 500 pounds and over as of January 1, 2016 totaled 19.8 million head. This is 3 percent above the 19.3 million head on January 1, 2015. Beef replacement heifers, at 6.29 million head, are up 3 percent from a year ago. Milk replacement heifers, at 4.82 million head, are up 2 percent from the previous year. Other heifers, at 8.71 million head, are 3 percent above a year earlier.

- All Calves under 500 pounds in the United States as of January 1, 2016 totaled 14.1 million head. This is 4 percent above the 13.5 million head on January 1, 2015. Steers weighing 500 pounds and over totaled 16.3 million head, up 4 percent from one year ago. Bulls weighing 500 pounds and over totaled 2.14 million head, up 2 percent from the previous year.

Calf Crop Up 2 Percent

- The 2015 calf crop in the United States was estimated at 34.3 million head, up 2 percent from last year’s calf crop. Calves born during the first half of 2015 were estimated at 24.8 million head. This is up 2 percent from the first half of 2014. The calves born during the second half of 2015 were estimated at 9.50 million head, 28 percent of the total 2015 calf crop.

- Cattle and calves on feed for the slaughter market in the United States for all feedlots totaled 13.2 million head on January 1, 2016. The inventory is up 1 percent from the January 1, 2015 total of 13.0 million head. Cattle on feed, in feedlots with capacity of 1,000 or more head, accounted for 80.2 percent of the total cattle on feed on January 1, 2016. This is down 1 percent from the previous year. The combined total of calves under 500 pounds and other heifers and steers over 500 pounds (outside of feedlots) is 25.9 million head. This is 5 percent above one year ago.

Download the full report: USDA 2016 Jan 1 US Cattle Inventory Report

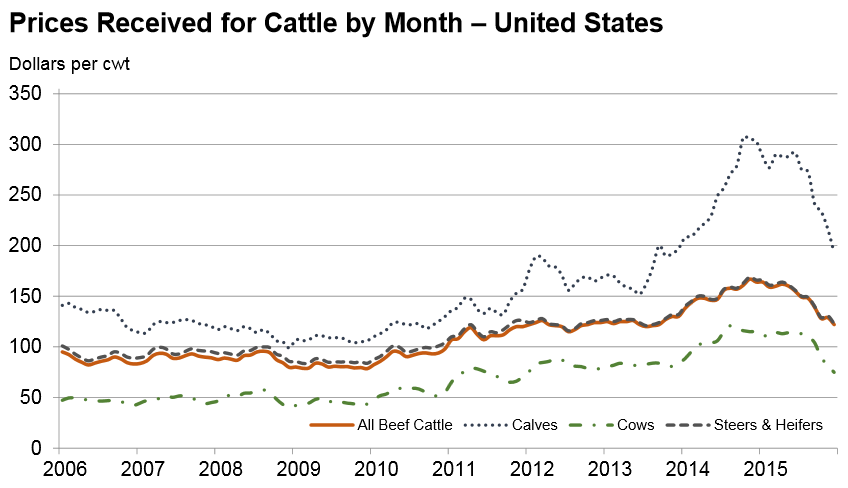

With the increase in inventory (supply) as well as the reduction in export demand, cattle prices are down significantly from the peak prices received at the end of 2014. Cattle prices fell much faster than they rose. There are many factors that affect the price calves sell for at your local auction, but it is clear that ranchers will have to work harder on efficiency to remain profitable in the years ahead. Cattle prices are currently headed in the wrong direction, but there are market factors that can change this over time. As retail beef prices begin to follow live cattle prices, perhaps there will be an increase in the demand that will help stabilize prices at a moderate level that can be profitable for the entire industry.

0

0